Since the United States abandoned the gold standard in 1971, the purchasing power of the U.S. dollar has fallen by more than 85 cents on the dollar.[1] The Canadian dollar has followed a similar trajectory. Meanwhile, gold, silver, and Bitcoin have served as hard-asset hedges — rising in price as fiat currencies are inflated away.

This page explains what currency debasement is, why it happens, how it has unfolded historically, and what practical steps you can take to protect your purchasing power. Data and sources are cited throughout.

What Is Currency Debasement?

Currency debasement occurs when the purchasing power of a monetary unit falls because the supply of that currency is expanded faster than economic output grows. In plain terms: more money chasing roughly the same amount of goods means each dollar buys less.

Modern debasement is digital. Central banks increase the money supply by crediting accounts — no printing press required. Between 2020 and 2022, the U.S. Federal Reserve expanded its balance sheet by roughly US$4.8 trillion,[7] the single largest monetary expansion in U.S. history. Canada's Bank of Canada similarly tripled its balance sheet during COVID-19 emergency measures.[8]

Ancient Origins

Debasement is not new. Roman emperors reduced the silver content of the denarius coin from 90% pure silver under Augustus (27 BC) to less than 5% by the reign of Gallienus (268 AD).[9] The result was runaway inflation, economic collapse, and eventually the fall of the Western Roman Empire. Medieval European monarchs clipped the edges of coins and restruck them with lower precious-metal content to fund wars. Every civilization that debased its currency eventually paid the price.

Why Governments Debase

A Brief History of Debasement

Understanding the historical pattern helps you recognize where we are today.

Core Hard Assets

Three assets have historically served as effective stores of value when fiat currencies depreciate. Each has distinct advantages, risks, and practical considerations for Canadian investors.

Gold has served as money for over 5,000 years. It is dense, durable, divisible, and universally recognized. Central banks hold over 36,000 tonnes globally,[2] making it the world's largest reserve asset outside of U.S. Treasuries.

Gold climbed from roughly US$1,225/oz in 2010 to over US$3,200/oz in 2025 — a 161% gain that far outpaced CPI inflation over the same period.[5]

Canadian investors can hold physical gold (coins, bars), gold ETFs (e.g., iShares Gold ETF, Sprott Physical Gold Trust), or gold mining stocks. Physical bullion held outside the banking system eliminates counterparty risk.

Silver is more volatile than gold but offers a dual hedge: it functions as a precious metal and as an industrial input in solar panels, electronics, and medical devices.[4] This industrial demand provides a floor that pure monetary metals lack.

The gold-to-silver ratio (how many ounces of silver buy one ounce of gold) has historically ranged from 15:1 to 100:1. When the ratio is high (silver relatively cheap), silver may be undervalued. In 2020 the ratio exceeded 120:1 before silver surged. Silver is accessible to smaller investors and available at most Canadian coin dealers.

Bitcoin is a decentralized digital asset with a hard cap of 21 million coins. No government, corporation, or individual can increase the supply — a feature deliberately designed as an antidote to fiat debasement.[3]

From roughly US$0.10 in 2010 to over US$90,000 in 2025, Bitcoin has been the best-performing asset class of the past 15 years by a wide margin.[6]

Bitcoin carries higher volatility than gold or silver, but also offers portability, divisibility to 8 decimal places (satoshis), and self-custody without need for any intermediary. Canadian exchanges regulated by FINTRAC include Bull Bitcoin and Bitcoin Well.

Real estate, farmland, commodities, and productive businesses also resist debasement — their nominal value tends to rise with inflation. However, they require larger capital, are illiquid, and carry specific risks (regulatory, tenancy, crop failure).

These assets are outside the scope of this page but are worth considering as part of a diversified approach. Always consult a qualified financial advisor before making significant investment decisions.

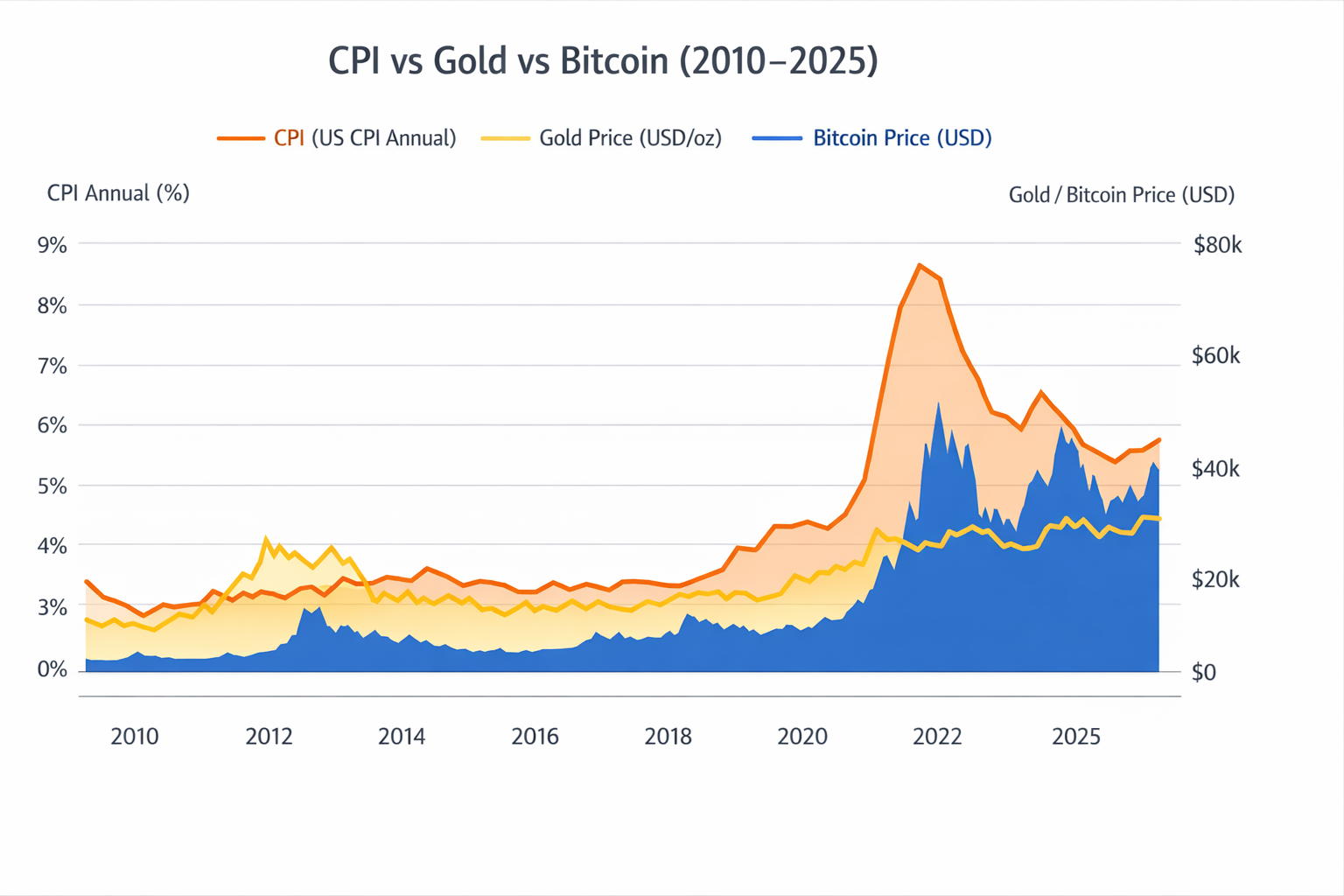

CPI vs Gold vs Bitcoin (2010–2025)

The table below shows annual CPI inflation (U.S.), the gold price in USD/oz, and the Bitcoin price in USD. Note the dramatic divergence: while consumer prices rose cumulatively by approximately 45% between 2010 and 2025,[1] gold rose 161%[5] and Bitcoin rose by many orders of magnitude.[6]

| Year | CPI (%)[1] | Gold (USD/oz)[5] | Bitcoin (USD)[6] |

|---|---|---|---|

| 2010 | 1.6 | 1,225 | 0.10 |

| 2011 | 3.2 | 1,572 | 6 |

| 2012 | 2.1 | 1,669 | 9 |

| 2013 | 1.5 | 1,411 | 200 |

| 2014 | 1.6 | 1,266 | 525 |

| 2015 | 0.1 | 1,160 | 272 |

| 2016 | 1.3 | 1,251 | 567 |

| 2017 | 2.1 | 1,258 | 4,000 |

| 2018 | 2.4 | 1,269 | 7,500 |

| 2019 | 1.8 | 1,393 | 7,200 |

| 2020 | 1.2 | 1,770 | 11,100 |

| 2021 | 4.7 | 1,799 | 47,000 |

| 2022 | 8.0 | 1,800 | 28,200 |

| 2023 | 4.1 | 1,940 | 28,900 |

| 2024 | 2.9 | 2,386 | 60,000 |

| 2025* | 2.8 | 3,200 | 93,000 |

* 2025 figures are estimates based on year-to-date data at time of publication. CPI: BLS CPI-U annual average.[1] Gold: LBMA PM Fix annual average.[5] Bitcoin: CoinGecko annual average.[6]

The Canadian Perspective

Canadian investors face a compounding currency risk that U.S. investors do not. When the Canadian dollar weakens against the U.S. dollar — as it has done repeatedly — the cost of imported goods rises even before domestic inflation is factored in. In early 2025, the CAD traded near US$0.68–0.70, near multi-decade lows.[8]

How to Protect Your Wealth

The following four steps are a practical framework for building an inflation-resistant position. They are educational in nature — not financial advice. Always consult a qualified advisor before making major financial decisions.

Allocate a portion of savings across gold, silver, and Bitcoin so that no single currency or counterparty risk dominates your portfolio. A common starting framework used by inflation-concerned investors is a small allocation (5–20%) to hard assets as a core hedge. The right percentage depends on your risk tolerance, time horizon, and existing assets.

For physical gold and silver: use a home safe, safety deposit box, or an allocated vault service. For Bitcoin: move coins off exchanges into a hardware wallet (Coldcard, Trezor, Ledger). Write down your seed phrase and store it offline in two separate physical locations. An exchange is not a vault — if the exchange fails, your coins may be gone.

Review your asset allocation once a year. When one asset class has significantly outperformed (e.g., Bitcoin quadrupling), selling a portion back into other assets or cash can lock in gains and maintain your intended risk level. Do not let a single position become so large that a 50% drawdown would be catastrophic for your financial life.

Monitor key macroeconomic indicators: central bank balance sheet size, M2 money supply growth, CPI trends,[1] and central bank gold purchases.[2] When debt levels are rising and real interest rates are negative (inflation higher than the interest rate on savings), hard assets historically perform best. Conversely, when rates rise sharply as in 2022, hard asset prices can fall temporarily.

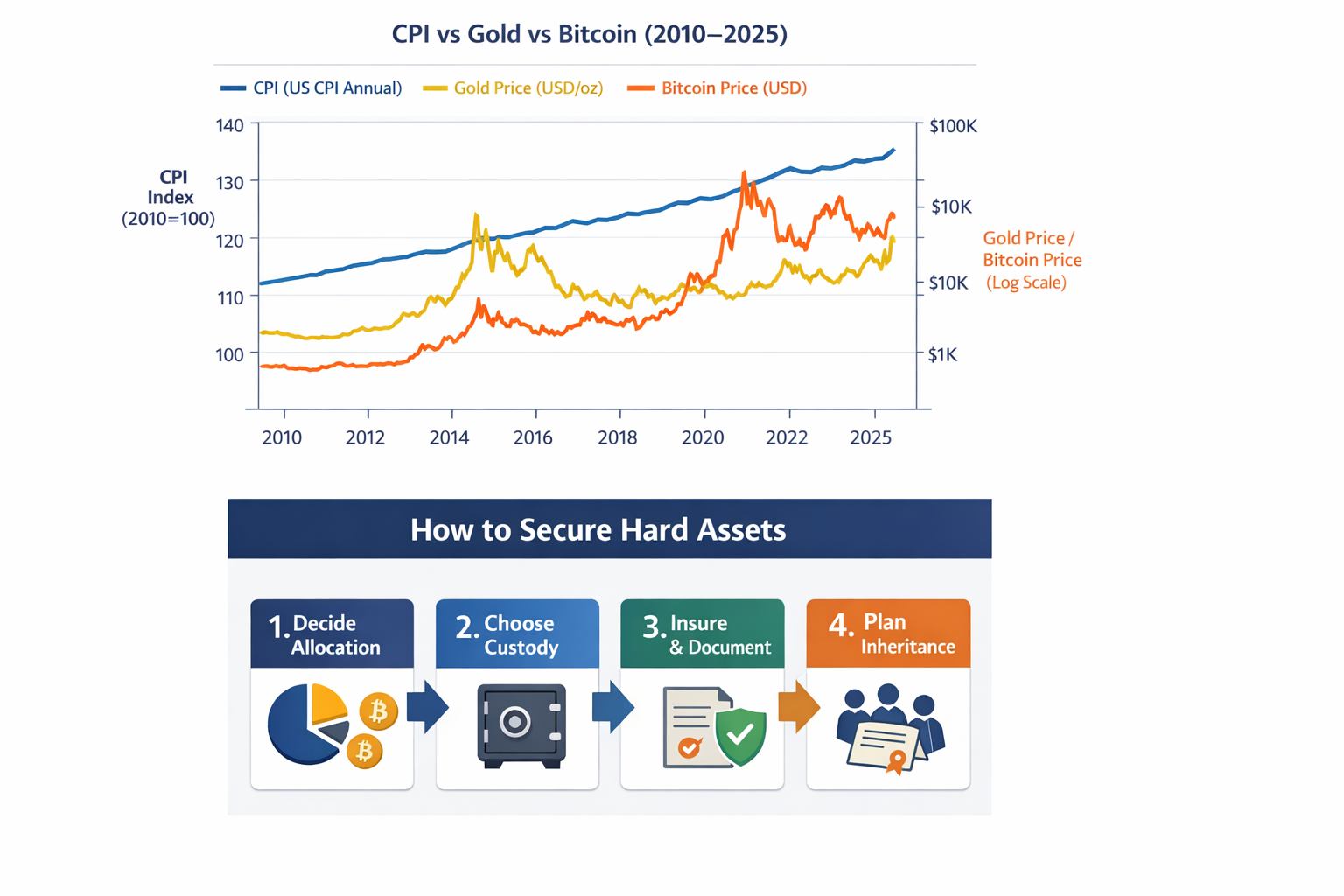

How to Secure Hard Assets

Physical and digital hard assets require different custody approaches. The infographic below outlines the four key steps: deciding your allocation, choosing your custody method, insuring and documenting, and planning for inheritance.

Risks and Counterarguments

A balanced view requires acknowledging the genuine risks of each hard asset hedge.

🍁 Learn More at Maple Bitcoin School

In-depth Canadian Bitcoin education — from self-custody and DCA to regulatory guidance and wealth-building strategies.

Join Maple Bitcoin School →Sources

All factual claims on this page are drawn from the following publicly available sources. Numbers in superscript throughout the page link to the relevant entry below.

-

1U.S. Bureau of Labor Statistics (BLS) — Consumer Price Index (CPI-U) annual data. bls.gov/cpi — Used for all CPI figures in the table and text.

-

2World Gold Council — Global gold market data, central bank holdings, and investment research. gold.org

-

3Investopedia — Bitcoin — Bitcoin overview, 21 million cap, and monetary design context. investopedia.com

-

4The Silver Institute — Silver supply, demand, pricing, and industrial applications data. silverinstitute.org

-

5London Bullion Market Association (LBMA) — Gold and silver PM Fix annual average prices. lbma.org.uk

-

6CoinGecko — Bitcoin historical price data and annual averages. coingecko.com

-

7U.S. Federal Reserve — Federal Reserve balance sheet data, M2 money supply, and policy history. federalreserve.gov

-

8Bank of Canada — Canadian monetary policy, balance sheet data, CAD exchange rate history. bankofcanada.ca

-

9Historical / General Reference — Roman debasement history (denarius silver content decline); Nixon Shock 1971 and Bretton Woods dissolution. Multiple academic and historical sources including Investopedia: Bretton Woods.

⚖️ Legal & Financial Disclaimer

For educational and informational purposes only. Nothing on this page constitutes financial, investment, tax, or legal advice. The author is not a licensed financial advisor, registered investment advisor, securities dealer, or tax professional.

No guarantee of accuracy or completeness. While every effort has been made to present accurate data from reputable sources, figures — especially those marked with an asterisk (*) — may be estimates, approximations, or based on year-to-date data at time of publication. Markets change rapidly. Always verify data independently before relying on it.

Past performance is not indicative of future results. Historical returns for gold, silver, Bitcoin, and any other asset discussed on this page do not guarantee similar returns in the future. All investments carry risk, including the risk of total loss.

Not a recommendation to buy or sell. Any mention of specific assets, exchanges, ETFs, or products is for informational illustration only. The author may personally hold positions in assets discussed on this page. This is not a solicitation to buy or sell any security or commodity.

Canadian tax obligations. The Canada Revenue Agency (CRA) treats Bitcoin, gold, silver, and most hard assets as property or commodities. Disposals may trigger capital gains or income tax obligations. Consult a qualified Canadian tax professional (CPA) before making any investment decisions.

Regulatory risk. Governments have historically imposed restrictions on gold ownership and may impose regulations on Bitcoin and other digital assets. Regulatory environments vary by jurisdiction and can change without notice.

Reliance at own risk. By accessing this page, you agree that you are solely responsible for any decisions you make based on the content herein. The author assumes no liability for any loss, damage, or adverse outcome arising from the use of this information. Always consult a qualified professional before making financial decisions.